- The Promote

- Posts

- A Lender Bender Special, Plus: Cushman Earnings, Multifamily 💀 & Policy Bites

A Lender Bender Special, Plus: Cushman Earnings, Multifamily 💀 & Policy Bites

Hiten Samtani

February 21, 2024

Lender Bender

“Maybe you could tell me what is going on. And please, speak as you might to a young child. Or a golden retriever 🐕️ . It wasn't brains that brought me here; I assure you that.” - John Tuld, “Margin Call”

We’ve run out of cushion. Bad CRE debt has exceeded loss reserves at the big banks, after a spike in late payments on several asset classes.

Average reserves at the 🐳 banks(JPMorgan, BoA, Citi, Goldman, Morgan, Wells) are now at 90 cents for every $1 of debt on which a borrower is at least 30 days late, per the FDIC. That’s down from $1.6/$1 in ‘22. Collectively, the 6 big banks saw delinquent CRE debt nearly triple to $9.3B.

“There are banks that may have looked fine 6 months ago, that are going to look not so good next quarter,” analyst Bill Moreland of BankRegData told the FT.

(Some readers requested an audio version of this thing. You can find it in the Soundcloud link above 👆️ - still raw but a start)

Some observers say that post-Covid, relying on historical loss rates is not enough – just look at the recent carnage in office – and that banks should adjust reserves (funds set aside to cover future losses) to account for current levels of delinquencies.

What's on tap - Feb. 21

Today’s sponsor is: BetterPitch

Whether raising an SPV, open-ended or REPE fund, lean on BetterPitch’s team of seasoned analysts, copywriters and designers to make your pitch professional and crisp. Focus on your core competency – real estate – and let us figure out how to make your pitch pop.

Get in touch today for a free pitch deck audit.

Lender CRE exposure (cont.)

“We need to see if the banks have been forward-looking in predicting expected losses, and not just relied on what has happened in the past,” UChicago’s João Granja told the FT.

Big banks maintain that CRE is not significant enough to their biz to be a problem. “It’s such a small part of the table,” BofA boss Brian Moynihan said in Dec., pointing to just $5B in CRE debt on the bank’s books tied to struggling asset classes. “We feel good.” This month though, the bank said delinquencies on CRE loans in some asset classes had jumped 50% in Q4 to $2.1B, while loss reserves had been cut by $50M to $1.3B.

“Any downturn in provisions would fundamentally be the wrong behavior” said CBRE’s top economist Richard Barkham, estimating that banks could lose up to $60B on bad CRE loans in the next 5Y - that’s 2x their loan reserves for that sector, per BankRegData.

Meanwhile, the problems are far more acute down the food chain. We’ve already seen the CRE-related carnage play out at NYCB, whose stock is down 55% YTD. Bloomberg has a sharp new analysis looking at mid and small-sized lenders’ CRE exposure, and how many of them (Valley National, WaFd, Axos) exceed regulators’ guidelines on exposure.

Bloomberg’s review found 22 banks with $10 billion to $100 billion of assets hold commercial property loans three times greater than their capital. Half of those firms had growth rates surpassing the thresholds laid out by regulators.

“We’re at the warning stage,” former acting comptroller of the currency Keith Noreika told the publication. “There’s a light going off on the dashboard and now people are opening up the hood to see: Is it really wrong or do we just need to keep our eye on it?”

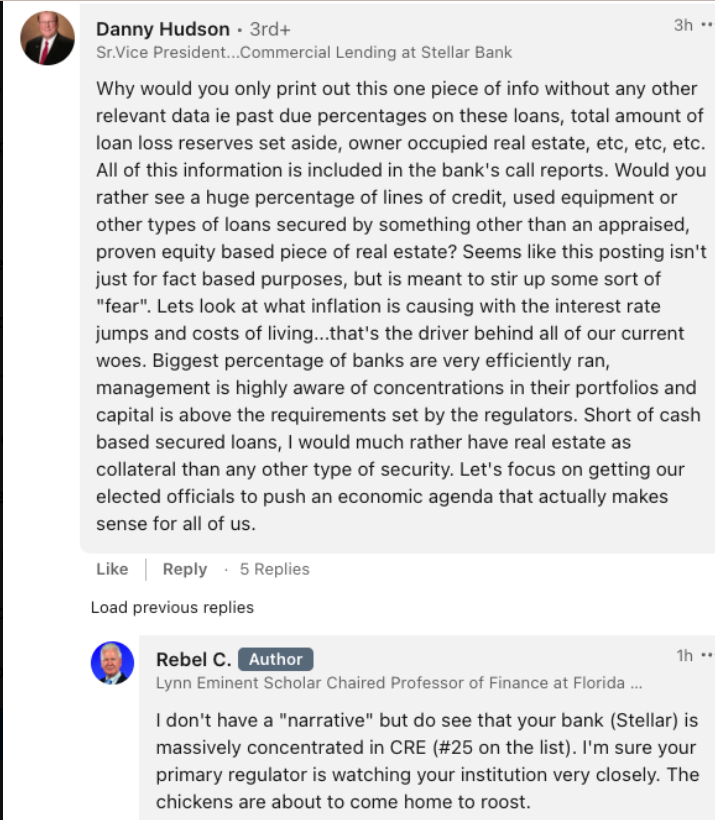

Rebel with a cause: FAU finance prof Rebel Cole published an analysis of CRE exposure (using the same FFIEC data) in which he took into account construction loans + unused commitments to fund CRE mortgages & construction loans. He ID’d 71 banks that have both $10B+ in assets and exposure that is > 2.5x equity capital. Here’s his top 10 (major condo construction lender OZK’s at #2) - see rest here

Lender exposure to CRE (Credit: Rebel Cole via LinkedIn)

Things got spicy when an exec at one of the lenders (Stellar Bank) on the list took issue with the analysis.

Credit: Rebel Cole via LinkedIn

🪰 on the wall: I enjoyed this conversation between a credit investor and a banking regulator 🔍️ on loan modifications, and particularly this insight: “just bc a loan is technically performing, does not mean it is good credit.” They also talked about “repacking reserves”- banks putting reserves up on borrowers’ behalf to keep the loan current.

Interesting parallel from the fund manager 🌎️ : Hodes Weill co-founder David Hodes says in PERE that it may be time to up the reserves (typically 10%) held by REPE fund managers. “Most assets probably need another 15-20% to address refinancing if they had to do it today based on current lender appetite for risk,” Hodes says.

Policy Corner

A few essential nuggets to bite into below:

SCOTUS dashes NY rent law challengers’ hopes: 2 more petitions to review the state’s ‘19 RS law (which many blame for pulverizing the market) were rejected Tuesday. The fat lady hasn’t 👩🎤 yet, however: Justice Thomas left the 🚪 open for a future challenge

Exclusionary zoning: A new 🗞️ makes the argument that restrictions on the amt. and type of housing developers are allowed to build is unconstitutional, bc it amounts to a “Taking.” You can DL it here.

Medicaid 🏥 pays the rent: “For more than a decade, researchers and advocates have argued that housing is a fundamental part of health care.” An excellent primer here from Vox on a pilot project to use federal Medicaid dollars to help with rent payments. Arizona and Oregon are first on the list, and New York, California, Hawaii, and Washington have all applied to avail of the Biden admin. program.

Going Greek at Farley

Greek hotspot Avra is coming to Vornado’s Farley Building (building photo via VNO)

Sea-and-be-seen. Greek seafood hotspot Avra, a favorite with the New York real estate set, is coming to Vornado’s Farley Building, signing for a massive 20K sf, per Cuozzo. The deal gives immediate culinary cachet to a part of Manhattan traditionally known for Sbarro vibes and sets Vornado up nicely to compete for foodie attention with Related’s Hudson Yards and Brookfield’s Manhattan West. Avra will be right by Meta’s 730K sf spread.

Nearby, Vornado is tabling its plans for a 2.7M sf skyscraper at the razed Hotel Pennsylvania site, per Crain’s, in favor of an 80K sf event space ( US Open 🎾, NYFW 👗 , etc.) and 10-story digital billboard. Business Insider, perhaps unaware that Vornado is the largest owner of signage space in Manhattan, opted to go with the “NYC's commercial real estate crisis is so bad that…” interpretation of the move. (BI’s RE coverage has been all over the place these past 18 months; they have talented reporters but seemingly little overall editorial vision for the vertical, whiplashing between “rising stars” type stuff, first-person adventures through the built environment and doom-and-gloom macro 😢 )

If you like what you’re reading, please consider subscribing here. And if you’re already subscribed, forward this to all your friends 🙏

Not-so-Cushy Gig

Cushman earnings dropped Tuesday: $2.6B revenue, $70M net income for the Q; $9.5B revenue, $35M net loss for the year. CEO Michelle MacKay focused on balance-sheet babysitting 👶 (deep dive here) in her earnings call and in the press release. The brokerage spent $56M over the year on “cost savings initiatives,” and achieved savings of $140M. Talk of growth was vague: “Every week, we hear about more funds being raised for real estate investments,” Mackay said, stressing that the priority was prepping to “capitalize when the market inevitably rebounds.” More here and here.

Multifamily Mania

Harbor Custom Development released details on its Chapter 11

1) Exit stage left: Tacoma-based multifamily developer Harbor Custom Development is bowing out. After filing for Ch. 11 in Dec., the company now plans to sell off its assets and submit a liquidation plan to the court, per the Puget Sound BJ. Shareholders are expected to be completely wiped out - the company reported $224M in assets and $173M in debts at the end of Sept.

2) Arbor 10K drop: Arbor Realty Trust released its 10K Tuesday, a couple days after its earnings call. Haven’t had the time to dive into it fully, but here’s an interesting snippet:

Also, Viceroy, the short seller that is targeting Arbor, went on the warpath on TRD’s Deconstruct pod this week. It then dropped a new memo on the lender post the 10K release, titled “Baloney with a side of flimflam.” It still feels to players I’ve spoken with that Viceroy doesn’t quite grasp the nuances of Arbor’s business, an odd position to be in when you’re trying to take down the company. (Arbor CEO Ivan Kaufman addressed the Viceroy campaign during earnings, describing it as “🍒 -picking data to “inject fear into the market for personal gain.”)

Unquotable Quotes

“The chief financial officer — you can only give the responsibility to someone who’s able to get it right.”

Favor

If you liked this edition of The Promote, the best thing you can do is tell people about it. Email it, text it, share snippets with your family and friends. We’re new, we’re having a lot of fun and we’d like everyone to participate. Check out this chat I did w Hunter on Friday if you want a sense of the broader vision for ten31 – that bit starts at 33:18. Subscribe here. Reach out for advertising here. And follow me on Twitter for more spice between the letters.